“Our income statement shows we’re making a profit, but it sure doesn’t feel like it.”

It was a contractor’s wife who had a pretty good feel for how their business was going.

“Why do you say that?” I asked.

“Our receivables and inventory are about the same, but I don’t have enough cash for payroll and bills. We’re behind with vendors, our credit card balances are up, we’re at the limit on our credit line, and our banker is asking questions. I think we need to charge more, but my husband says as long as we’re making a profit, I shouldn’t worry.

But I do worry. A lot. Something’s wrong.”

"The P&L and the math are simple, but depending on how they’re prepared, P&Ls can show wildly different results."

We all know what an Income Statement is, although we may call it a Profit and Loss (P&L). It’s the statement that tells us whether or not we’re making money.

To create the report, we add up the sales for a period, usually a month or a year, then subtract all the expenses for the same period.

A positive remainder is profit, a negative remainder is a loss. Simple enough, right?

Well, yes, and no.

The P&L and the math are simple, but depending on how they’re prepared, P&Ls can show wildly different results. To get an accurate, useful report, we have to understand what goes into it and why it matters. My experience as a business coach has shown that there is a lot of confusion about that.

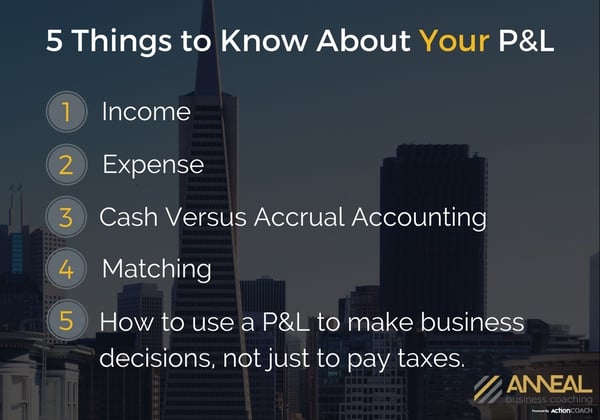

Through years of looking at small business P&Ls, I’ve found five concepts contribute most to the confusion. Small business owners who are unaware or unfamiliar with the concepts do not benefit from timely, accurate information that is critical to their prosperity.

NOTICE: An accountant may take exception to the discussion below due to concerns about precise definitions and subtleties. However, most of us are not accountants. There would be little to gain from lengthy refinements to explain every accounting exception and nuance.

Income is money (or the promise to pay us money) we receive from selling our product or service. It does not include money we receive from the sale of assets such as a building, or from loans or investors or that we contribute to our businesses.

Most of us are pretty clear about that.

Expense is cost we incur to get sales and includes things like rent, sales commissions, and the inventory we sold. Most of us understand that, but I often see things like income taxes and truck payments shown as expenses, which they are not.

Expenses are a little more complicated than sales because there are two kinds of expense, Cost of Goods Sold and Overhead. It is important to know the difference.

Cost of Goods Sold goes up and down with sales. For example, if we double our sales in a month, our Cost of Goods Sold would also double. Cost of Goods Sold expenses are things like job material, sales commissions, and freight.

Overhead expenses do not go up and down with sales. If we double sales in a month, or even if we had no sales, overhead expense would remain the same. Overhead includes things like office salaries, rent and phone service.

Although both Cost of Goods Sold and Overhead are expenses, it is important to separate them on the P&L.

We’ll see why below.

A P&L can be prepared on either the Cash or Accrual basis. Cash basis means that we don’t include sales or expenses until they have been paid. Accrual means we include all transactions at the time the time they happen.

It’s not hard to imagine that an accrual basis report which includes all transactions might be very different from a cash basis report which ignores sales and purchases made on account.

It was this issue that confused and mislead the my contractor and his wife.

After a quick look, I saw that Quickbooks was reporting their P&L on the cash basis. Fortunately, they kept good books which made it easy to convert the report to accrual with one click of the mouse.

The differences were huge: the cash P&L showed a $26,000 profit for January, the accrual report showed a $56,000 loss.

"The differences were huge: the cash P&L showed a $26,000 profit for January, the accrual report showed a $56,000 loss."

With the problem explained, we could get to work correcting it.

The accrual method is far more accurate than the cash method. As managers of our small businesses, we have to have our reports prepared using the accrual method.

“But my accountant says I’m on the cash basis!” you say. Your accountant is referring to how you calculate your taxes. Accountants can easily compile cash basis tax returns from accrual based books. They cannot, however, compile accrual based reports for us from cash based books.

I said above that a P&L compares income and expenses for the same period.

That’s a big deal.

In some businesses, like retail, expenses and sales are easy to record in the same period. In other businesses, like contracting, it’s not so easy. I often see reports from contractors that show wild swings in profitability from month to month.

"Over long enough periods, these monthly swings tend to dampen out, but we can’t wait a year to find out if we made money last month."

Say you’re a contractor and you spend money on material and labor in June and get paid in July. June would look horrible, July would look fantastic, but neither report would be accurate.

Or let’s say your liability insurance for the next 12 months is $48,000, and you pay the whole bill in January. That’s a big hit to January’s P&L that should have been spread over the year at $4,000 per month.

Over long enough periods, these monthly swings tend to dampen out, but we can’t wait a year to find out if we made money last month.

The quality of our decisions improves with the quality of information and insights available to us. A proper P&L statement is an abundant source of both. The highest and best use of a P&L is to help us make business decisions about the future. A proper P&L is essential for two reasons:

"The quality of our decisions improves with the quality of information and insights available to us."

Misinformation and instincts were leading my contractor toward disaster. He wouldn’t listen to his wife until he was convinced they were losing money.

Once he knew the real score, he was motivated to act.

The P&L can provide the score to get us motivated AND a running score to tell us how well our adjustments are working if - and only if - it is accurate and timely.

The P&L is an abundant source of ideas and information to guide our decisions. One of the most useful features of a proper P&L comes from separating Cost of Goods Sold from Overhead expenses, which allows us to calculate margins.

To see how margins can guide our decisions, see my articles “The Most Important Number in Business” and “How to Build a House for free.” As you read the articles, notice that none of the amazing results would be possible without a proper P&L prepared using the five concepts.

Discussing the five concepts is not the same as putting them into practice, but understanding begins with awareness. Now that we are aware, we can talk with our accountant about the five concepts to be sure our P&Ls are prepared using:

Correct Income

Correct Expenses, separated into Cost of Goods Sold and Overhead

Accrual based methods, and

Proper Matching

How do you judge if you’re making money or not? How often do you see your P&L How do you make business decisions? How do you measure the effectiveness of your decisions? How do you keep score?

Thank you for reading this article. As always, I value your opinion and welcome your comments and suggestions for future articles in the comment box below.

.jpg)

.jpg)

.jpg)

.jpg)

{kind=link}