“It’s me Martin. It’s all me.”

“How far back should I go?”

“January.”

I went back to January, but I didn’t stop there. By the time I’d been through five years of bank statements, I had found more than $340,000 missing, stolen by the most trusted member of our management team, our in-house bookkeeper. In the end, her father paid back the money, but she got jail time and ruined not only her life, but the lives of those most dear to her as well.

Our bookkeeper stole from us through a very simple process: She paid her credit cards online using our bank accounts. I didn’t catch on because her credit cards had the same name as ours on the bank statements, and I didn’t notice the different account numbers until she took a very large sum in one month.

"Looking back, there were many signs I should have noticed, but didn’t."

Although she made the decision to do it, I allowed the environment that made it possible for our bookkeeper to steal from us. I could have prevented the theft but I didn’t, and for that reason I am at least partly responsible for ruined lives. It is our responsibility as business owners to prevent embezzlement from happening. Not only for the sake of our companies (I think back to the many times I could have used that $340,000!), but also for the sake of ruined lives.

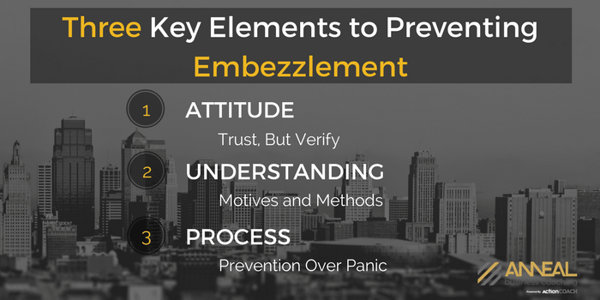

And before you think embezzlement is unlikely in your business, let me point out the fundamental key to preventing embezzlement: Don’t think it won’t happen to you. (That attitude is known as Optimism Bias. Read more about how it undermines executives here.)

Ask around and you will find that embezzlement in business is as common as grass on the prairie.

So common, in fact, that the detective scoffed at my meager $340,000 claim. He told me his white collar crime division had enough multi-million dollar claims to consume the department’s entire resources into the foreseeable future. The only way they would pursue my case was if I would lay out the facts and evidence in foolproof detail, which I did.

But all too often embezzlement goes undetected and tracks have been covered well, making foolproof detail unlikely, and a foolproof case with compensation even less likely.

This is why the time and energy put into the prevention of embezzlement can save your business and employees a lot of loss in the end.

We all should adopt that old Russian proverb as our guiding philosophy. We have to maintain the attitude that embezzlement is not only possible, but likely, because it is. Everyone in our organizations should know we are constantly looking and have procedures in place to prevent theft. It’s not personal. It’s just the way it is.

Zero tolerance. Adopt the attitude that theft is theft. It doesn’t matter if it involves many thousands of dollars or a meal charged on the company credit card. Our attitude is that theft is theft and we will not tolerate it.

The vast majority of embezzlers don’t intend to become thieves and almost always start out small. The employee, as happened with my bookkeeper, has a family emergency and takes a few hundred dollars with the intent to pay it back. She pays back a little, but over time “forgets” to pay back the balance. Nobody notices, and something else comes up. She takes a little more, still intending to pay it back. Again, nobody notices. Over time, she drops all pretense of “borrowing,” and family emergencies become clothes, vacations and cars.

Those of us who don’t think like thieves are often surprised at the methods people use to embezzle. We are even more surprised at how easy it is. Below are a few examples of embezzlement provided to me by friends. If you are familiar at all with basic accounting controls, these will all seem pretty simple and dumb. They are, but they worked.

One embezzler set up a company with a name similar to his employer. When customers paid their accounts, he deposited the checks to his dummy company and deleted the original sales transaction from Quickbooks. Poof! Transaction and money were gone.

A bookkeeper responsible for payroll paid her boyfriend $600 per month as contract labor for work he didn’t do. He never even showed up to work.

This is so common, it’s almost universal. The employee buys gas, or supplies or material for personal use on the company account.

An employee working with someone at a supplier business, accepts and pays phony invoices for material or services never received.

A manager with complete signing authority set up maintenance and landscaping companies to care for the properties she managed. The companies overcharged over $300,000 for work not done.

It is harder these days because so many payments are made with cards and transfers, but cash regularly disappears from restaurants, bars and convenience stores. The most common method is to pocket cash for transactions that are not rung up.

I would have noticed my bookkeeper’s thefts had she entered them as expenses in the current month. She didn’t. She entered the “expenses” in prior years, then transferred them back at year end. I didn’t notice the charges after they had been transferred back because the amounts were not noticeable in large annual totals.

Most of the examples above could have been prevented by simply paying attention. However we seldom have time to monitor every credit card transaction, check, bill and receivable.

We don’t have time to haphazardly review transactions, but we can and must find the time to install anti-theft processes and to devote several hours each month to review a few critical reports. Below are some of examples of basic processes used to prevent or catch embezzlement.

.png?width=600&height=300&name=Embezzlement+Prevention+Checklist+(1).png)

At the absolute, bare minimum we have to reconcile our bank accounts every month. Without reconciled bank statements, we have almost no chance of spotting theft. To be effective, we have to reconcile every month, while charges and deposits are fresh in mind.

If we are unable or unwilling to reconcile our own bank accounts, we have to find someone to do it for us, but that someone should NOT be the person who pays bills. The best option is to have an outside accountant do it for us.

Credit cards are just like bank statements and should be reconciled for the same reasons. Again, the cards should not be reconciled by the same person who makes charges or who pays the credit card bills.

This is the most important defense of all. “Good books” means double entry, accrual based books such as Quickbooks, and keeping good books includes reviewing the information they provide.

Reviewing and closing books on a monthly basis is a rarity in small business, but it provides the best possible systematic process for reviewing transactions while they are fresh in mind.

Closing books makes it very difficult for embezzlers to backdate transactions, as my bookkeeper did, or to delete past transactions to cover theft. Reviewed books also keep us current on the state of our businesses (and banks love it!).

Every transaction in business begins with a “source document.” At a minimum, we need receipts for all expenses that show what was purchased, not just where it was purchased.

The person who does our invoicing should not receive payments on account. The people who enter our bills should not pay the bills. The person who receives cash should not be the one to deposit it.

We should all guard our signature authority closely. Signature authority applies to paper checks, bank transfer authority, and whatever other authority permits people to transfer money from our bank account.

Paying bills should be a formal process. Good books enable us to print accounts payable, which we review and choose the bills to pay.

Good books enable us to print aged accounts receivable listings which we should review at least monthly.

For harried small business owners, that sounds like a lot. But, it really isn’t.

Most of us can do it by establishing a few procedural changes and devoting a few hours a month to reviews. It is simple when it becomes routine. Work with your accountant to develop the right procedures for your business.

Our obligation to prevent theft extends beyond our duty to ourselves and our companies to include our obligation to prevent people from ruining their lives. Everyone has to know we are always looking. It is just the way we do things around here and we’re not changing.

Was this article useful? Do you have that sinking feeling that someone is stealing from you? Do you have the controls in place to prevent or catch embezzlement? Would you sleep better if you had processes in place? As always, I appreciate your questions and feedback in the comment box below.

.jpg)

.jpg)

.jpg)

.jpg)

{kind=link}