Could you imagine Russell Westbrook, the 2017 NBA MVP, playing without a scoreboard?

"As a business coach, I’ve noticed that owners, like Westbrook, manage their businesses differently when they understand the score."

No doubt he would always play hard, but he plays differently when he knows the score. We know that because during crunch time he is constantly checking the scoreboard for the score, fouls, time remaining, time outs - the information he needs to manage his game.

The Balance Sheet is the ultimate scoreboard for business.

As a business coach, I’ve noticed that owners, like Westbrook, manage their businesses differently when they understand the score.

The Balance Sheet is a list of what our businesses own and what they owe. If all it did were list those items, it would be invaluable, but it does much more than that.

The idea behind the balance sheet is that everything a business owns, its assets, is owed to someone. If the obligation is to a non-owner, such as a bank or a supplier, it is called a liability. If the obligation is to an owner, it is called equity.

Because everything is owed to someone, total assets must always equal the combined total of liabilities and equity. In other words, the two totals must “balance.”

Equity, or net worth, is our share. It is what’s left over after we subtract liabilities from assets. Equity is the “what’s left over” part because all non-owners out rank owners. They get paid before owners get anything.

We saw in my last article, “5 Things You Need to Know About Your Income Statement,” that income statements report on changes to income and expense accounts over a period of time.

The balance sheet reports on the overall condition of our companies at a point in time. Where the income statement guides operational decisions, (see “The Most Important Number in Business,”) the balance sheet guides the more strategic decisions that make operations possible.

"Where the income statement guides operational decisions, the balance sheet guides the more strategic decisions that make operations possible."

Through an ingenious process devised centuries ago, the balance sheet combines information from the income statement with information from asset, liability and equity accounts to provide a “snapshot” picture of our businesses.

It is a fascinating report that shows the cumulative effect of every transaction in the history of the business from inception through the time of the report. Changes in net worth over time reflect the ultimate score for how well we’ve run our businesses.

At a minimum, the balance sheet:

*Before we look at the balance sheet itself, it’s worth mentioning that the “things” we own or owe can be tangible or intangible.*

We all know that a truck is tangible. We can touch a truck and we can own one. Accounts receivable are intangible. We can’t touch them, but we can own the right to collect money, which makes accounts receivable assets.

All liabilities are intangible because they are all obligations.

Balance Sheets are arranged in a conventional order with Asset accounts listed first, Liability accounts second, and Equity accounts last.

Within each group, sub accounts are listed in order of liquidity. Liquidity is a measure of how fast the account is likely to provide or consume cash.

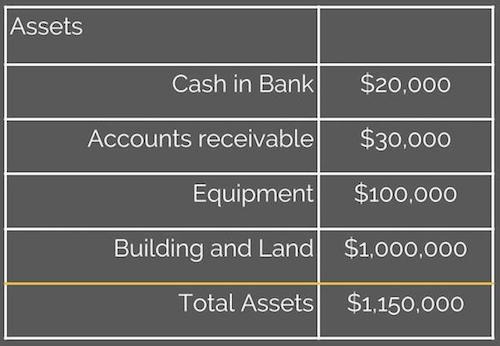

For example, the account “Cash in the Bank” is something we own and it IS cash, so it is listed first among assets.

The next item is usually Accounts Receivable, and the presumptions are that they are due soon and that people will pay us quickly, thus quickly converting accounts receivable into cash (They will pay us quickly, right?)

Inventory usually comes next, followed by equipment such as trucks, and finally by long-term assets such as buildings and land which are not easy to quickly convert into cash.

The Asset portion of the Balance Sheet might look like this:

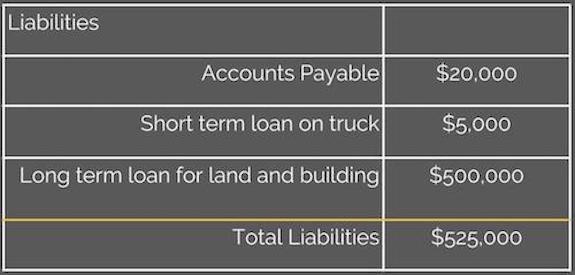

After assets come liabilities, also arranged in the order of liquidity. Accounts Payable is usually listed first among liabilities because suppliers expect to be paid pretty soon and it takes cash to pay them.

After accounts payable come short term loans due a few years out, such as loans for vehicles.

Last are longer term debts such as mortgages for land and buildings.

The Liabilities portion of our Balance Sheet might look like this:

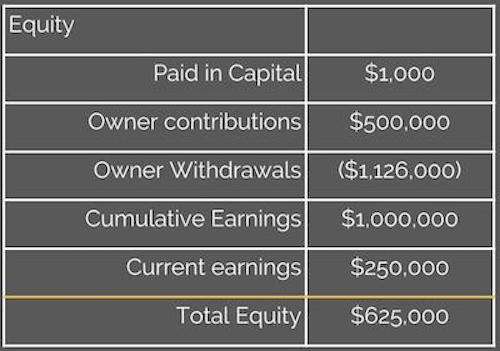

The final group of accounts are the equity accounts. These are arranged in a conventional order.

First is paid in capital, which is the original amount the owners paid in to start the company. I don't know why this is kept separate but it most often is.

Paid in capital is followed by a capital contributions account that keeps track of additional money paid by owners, which is followed by an Owner Withdrawal account that shows how much the owners have taken out of the business. Sometimes the additional paid in and taken out accounts are combined into one account that nets out the two numbers.

The final two Equity accounts are Cumulative earnings and Current Earnings. Cumulative Earnings show the total net profit or loss since the business began up to the beginning of the current year.

The Equity portion of our Balance Sheet might look like this:

Putting all three groups together without the details, we get a balance sheet that looks like this. We can see that all is right in the world because total Assets equals the total of Liabilities and Equity.

It is not likely that our balance sheets will be this simple, but as long as we understand Assets, Liabilities, Equity and the order of liquidity, we should be able to understand what we are looking at.

The Balance Sheet provides a lot of information just by looking at it, but it is more than just a list.

With a few calculations, the report provides valuable insights about our businesses by making the Statement of Cash Flows and ratios possible. (Don’t worry, YOU don’t have to make any of the calculations yourself. Quickbooks or your accountant will do them for you.)

The Statement of Cash Flows is the subject of another article, but is a critically valuable report that tells us where our cash went.

"Without a balance sheet, you’re not likely to get a bank loan, sell your business or even understand if you really made a profit."

Ratios, of course are some number divided by another number expressed as, for example, “Profit per dollar of Equity.” It turns out that ratios can tell us a lot of things that will help us guide our businesses.

Ratios can tell us our Return on Investment (think of ROI as equivalent to interest rate you receive on a dollar deposited in a bank). They can tell us how often we turn over our inventory (a measure of efficiency), how long our Accounts Receivable go unpaid (very important for managing cash flow), our debt “coverage” (a measure of how easily we can pay our debts without undue stress).

The balance sheet and ratios can also tell us our working capital requirements, which is very important information if we plan to grow our businesses (To see why see my article “Do You Know Why You are in Business?”

The list of potential uses for our balance sheets far exceeds those I’ve listed but let’s not forget to mention you’re that not likely to get a bank loan, sell your business or even understand if you really made a profit without one.

Do you have an accurate balance sheet for your business? Could you write out quickly and accurately what you own, what you owe and your net worth? Do you know how many assets you would need to double your sales? Could you present an accurate balance sheet to your bank?

As always, I appreciate your reading this article. Is there a topic you’d like to learn more about? I welcome your suggestions and comments in the comment box below.

.jpg)

.jpg)

.jpg)

.jpg)

{kind=link}